A Quest For Gold and Silver Profitability

Commodities / Gold and Silver 2013 Aug 24, 2013 - 12:23 PM GMTBy: Richard_Mills

There's an interesting interview done by Geoff Candy over on mineweb. com. In the interview Geoff asks Gold Fields CEO, Nick Holland "What went wrong with the gold industry?" Holland's reply is very informative.

There's an interesting interview done by Geoff Candy over on mineweb. com. In the interview Geoff asks Gold Fields CEO, Nick Holland "What went wrong with the gold industry?" Holland's reply is very informative.

"I think if you go back to the late '90s when gold was at a low of about $250 per ounce the industry at that time was really hanging on by its teeth and in order to do so was high grading and if you look at the average grades companies were mining it exceeded the reserve grade and that was never sustainable.

The other thing is exploration was cut back quite a lot and there's typically a timeframe of anything up to ten years or even longer between initial grassroots exploration and discovery and construction of a new mine. We're seeing the impact of some of that coming through the lower grades, grades have been declining steadily over the last ten to 20 years, against that backdrop we've seen cost inflation on a per ton basis - if you take out the grade effect - of anything between 10% to 15% per annum. That compounded means you would double your costs in five years, four to five years you'd double your costs. If you've got a grade decline on top of that you can see the overall impact on your total cost of producing an ounce."

A cash-cost standard was introduced by the Gold Institute in the 1990s and adopted by the gold mining industry. Cash operating costs only include:

- Direct mining costs

- Third-party smelting

- Refining and transport costs, minus byproduct credits

Using minimal cash cost accounting was once beneficial to a hurting industry, but over the last few years this minimalist reporting metric has hurt investors and gold miners in two significant ways:

- Cash cost reporting masks massive production cost escalation and almost flat profit margins despite gold's price rise

- The gold mining sector was targeted for new and higher taxes and royalties based on expected but unrealized profits

Using a different, more encompassing method of reporting costs would give investors a better, more accurate picture of the entire industry's profitability.

All-in metrics would count expenses such as:

- Sustaining capital

- General and administrative expenses (G&A)

- Exploration expenses

- Royalties - other than profit-based royalties

- Production taxes

- Total production costs which add in depreciation, amortization and reclamation and mine closure costs

An "all-in" cost measure would highlight the more investable, higher grade gold equities with better sustainable margins able to withstand the ups and downs of a cyclical industry with volatile prices.

A complete breakdown of costs, an "all-in" cost figure, courtesy of CIBC, shows cash operating costs pegged at $700 an ounce. Sustaining capital, construction capital, discovery costs and overhead at $600. Add in $200 for taxes and you get US$1500.00 as the replacement cost for an ounce of gold.

Scotiabank calculates "full cost reporting" (all-in cost plus development capital), at US$1,458 per gold oz for the companies it covers.

"Complete cost reporting" is full cost plus corporate taxes, it's forecast for 2013 at an average of US$1,690 per oz. gold.

Dundee Capital Markets reported that the average all-in cash cost in Dundee's silver equities coverage universe was $22.96 per ounce during the second quarter. Dundee's all-in cash cost calculation includes: site operating costs, exploration, corporate G&A, interest costs, royalties, taxes and sustaining capital.

Using the all-in figure provides a more accurate and definitive picture of actual mining cost and profit.

Below is a graph and a snippet from an excellent interview Joachim Berlenbach did with The Gold Report...

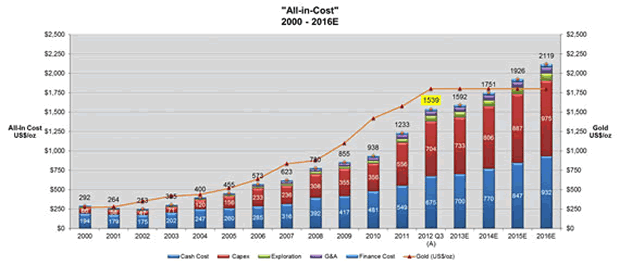

Joachim Berlenbach: "This graph includes all of the costs that make up a company's free cash flow: operating cash costs, sustaining capital expense (capex), expansion capex, exploration and finance costs, plus a bit of general and administration expense (G&A).

Total costs are sitting at $1,600/oz for the 13 biggest companies, which has been our universe for the last 13 years. Over the last two to three years, we have seen total costs rise an average of 15-17%. At a gold price of $1,600/oz, the industry does not produce a single Dollar of free cash flow. If we take a cost inflation of only 10%/year, we will need a gold price over $2,000/oz to maintain production..."

World Gold Council

For a long time the World Gold Council (WGC - the industry backed group that promotes gold), has been pushing gold miners to introduce a consistent all-in costs measure - a task force has been examining the issue in an attempt to create a standardized reporting format for the industry.

"It is expected that these new metrics, the "all-in sustaining cost" and the "all-in cost" will be helpful to investors, governments, local communities and other stakeholders in understanding the economics of gold mining. The "all-in sustaining costs" is an extension of existing "cash cost" metrics and incorporate costs related to sustaining production. The "all-in costs" includes additional costs which reflect the varying costs of producing gold over the life-cycle of a mine. It is up to individual companies to determine how they report to the market and to decide whether their stakeholders will find these new metrics of value in understanding their businesses; it is expected that, since many companies report on a calendar year basis, they may choose to use these metrics from 1 January 2014." World Gold Council

Gold production will drop

The underlying financial health of any company depends on ongoing profitability - sustainable margins.

In a quest to improve their bottom line gold mining companies are:

- Cutting jobs

- Deferring capital expenditure programs

- Cutting exploration

- Shutting down or selling uneconomic mines - ie Barrick plans to sell, close or trim production at 12 of its 27 mines where costs are higher than $1,000 per ounce

- Cutting dividends

- High grading

"In the coming months, we will see a huge effort by the industry to reduce costs. To become profitable again, the industry has to increase cash flow. To do this, a company could write off or stop capital projects already committed to. Instead of investing, it will try to preserve its free cash flow...

The industry also could go back into high-grading the ore bodies. High-grading means picking out the high-grade parts of an ore deposit to reduce costs in the short term. I saw this happen when I worked in the South African gold industry at the end of the 1990s. The gold price was below the breakeven price. Companies stopped exploration and started high-grading.

In the short term, high-grading might result in more profitable mines and better cash flow. But in the longer term, it means that we cannot mine enough gold. Gold production has not increased over the last 10 years, despite the rising gold price; it remains at 2,600 tons, or 80 million ounces (80 Moz), per year. If companies do not invest in new mines, gold production will drop drastically." Joachim Berlenbach, The Gold Report

Conclusion

Gold miners (and their investors) stark reality is that the capital costs of construction (Capex) and the daily cost of operations (Opex) have escalated significantly.

An investor into the gold mining space has to look at the space from a bottom up perspective - on a mine-by-mine, company-by-company basis. Questions need to be asked regarding reporting metrics to find the outstanding gems that still exist in the space.

Leveraging into a few good junior gold and silver companies owning the better precious metal projects should be on all our radar screens. I've got a few on my screen, but then I'm ahead of the herd. Are you AOTH?

If not, maybe one should be.

By Richard (Rick) Mills

If you're interested in learning more about the junior resource and bio-med sectors please come and visit us at www.aheadoftheherd.com

Site membership is free. No credit card or personal information is asked for.

Richard is host of Aheadoftheherd.com and invests in the junior resource sector.

His articles have been published on over 400 websites, including:

Wall Street Journal, Market Oracle, USAToday, National Post, Stockhouse, Lewrockwell, Pinnacledigest, Uranium Miner, Beforeitsnews, SeekingAlpha, MontrealGazette, Casey Research, 24hgold, Vancouver Sun, CBSnews, SilverBearCafe, Infomine, Huffington Post, Mineweb, 321Gold, Kitco, Gold-Eagle, The Gold/Energy Reports, Calgary Herald, Resource Investor, Mining.com, Forbes, FNArena, Uraniumseek, Financial Sense, Goldseek, Dallasnews, Vantagewire, Resourceclips and the Association of Mining Analysts.

Copyright © 2013 Richard (Rick) Mills - All Rights Reserved

Legal Notice / Disclaimer: This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified; Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

Richard (Rick) Mills Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.