The Corporate Cash Myth, What About Debt?

Companies / US Debt Dec 15, 2011 - 02:20 PM GMTBy: Neeraj_Chaudhary

A central theme that has absolutely permeated the coverage of the Great Recession is that over the past few years US corporations have cautiously hoarded cash and have stubbornly refused to invest in corporate expansion. Some have described this as a nearly irrational timidity on the part of the private sector and has for many justified the currently robust intervention from the public sector in the form of deficit spending, fiscal stimulus and monetary accommodation. The saying goes that if companies won't spend, government must pick up the slack to restart the economy. The story has been repeated so frequently and so often, that its veracity is rarely questioned.

A central theme that has absolutely permeated the coverage of the Great Recession is that over the past few years US corporations have cautiously hoarded cash and have stubbornly refused to invest in corporate expansion. Some have described this as a nearly irrational timidity on the part of the private sector and has for many justified the currently robust intervention from the public sector in the form of deficit spending, fiscal stimulus and monetary accommodation. The saying goes that if companies won't spend, government must pick up the slack to restart the economy. The story has been repeated so frequently and so often, that its veracity is rarely questioned.

The idea of "do nothing" corporations shirking responsibility fits neatly with the rhetoric coming out of the "Occupy Wall Street" movement which condemns the wealthy for doing little to help the economy. As proof of the story, many have pointed out that corporations have amassed a war chest on the order of $2 trillion. It is argued that millions of American jobs could be created if this money were to be put to work expanding corporate operations.

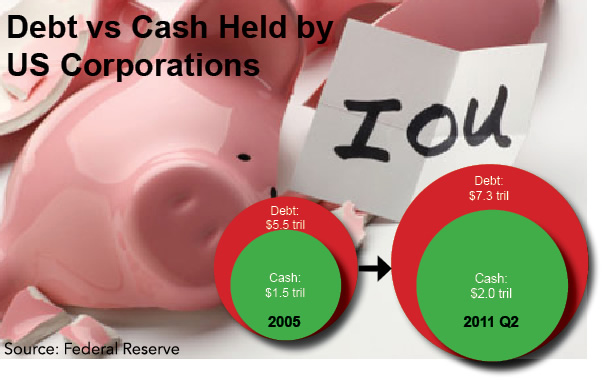

Unfortunately, facts have a pesky habit of mucking up an otherwise well tailored story. While it's true that US corporations have a record amount of cash on their books, as is widely reported, they are also carrying a record amount of debt, which is hardly reported at all. The chart above tells the story succinctly. Since 2005, U.S. corporations have added a half a trillion dollars of cash to their balance sheets. While that sounds like a lot, they have simultaneously added more than three times that ($1.8 trillion) in debt. Given the exposure that the debt creates, carrying large cash reserves should be viewed as an act of fiscal responsibility rather than unnecessary frugality. Sadly, like the rest of our struggling republic, many American companies are on the ropes, perhaps one good punch away from a knockout. With a high percentage of consumers and all levels of government still drowning in debt, it's very fortunate that at least one sector has cash in reserve.

To be clear, high levels of corporate debt is nothing new in the United States, where leverage has been on the rise since at least the early 1950s. But in recent years the trend has accelerated dangerously, most likely driven by the same factors that are encouraging debt in other sectors, namely a distortive tax code and artificially low and distortive interest rates.

On the tax side, two factors that have helped play a key role in this story are the double taxation of dividends by the federal government, and the deductibility of interest expenses.

All corporations pay taxes on their income, typically at a rate of 35%. Out of what remains, many pay dividends to shareholders. But once a shareholder receives that dividend, it is taxed again (most taxpayers pay a rate of 15% on qualified dividends). The fact that the same dollar of corporate income can be taxed at two different times reduces corporations' preference to raising equity when seeking to expand their business. Additionally, when a business takes out a loan or issues debt, the interest payments made to the lender or bondholder are generally tax-deductible. Together, the double-taxation of dividends and the tax-deductibility of interest expenses incentivize corporations to take on debt rather than issuing equity when they need to raise capital.

Of course, these factors have been in place for many years, and yet for much of that time, corporate debt remained within a fairly narrow range. In 1952, debts of nonfinancial US businesses amounted to roughly 30% of GDP. By 1981, these debts had reached about 50% of GDP; a bit on the high side, but certainly not terminal.

The variable that has likely caused corporate debt to balloon is the zero percent interest rates that have been, and will continue to be, the policy of the Federal Reserve for years to come. This ultra cheap money has made debt creation nearly irresistible.

It is the Greenspan-Bernanke policy of historically low interest rates that has provided a catalyst for higher borrowing in recent years. When Alan Greenspan took over as Chairman of the Federal Reserve in 1987, the ratio mentioned above stood at approximately 60%. After dipping briefly in the 1990s, corporate leverage took off in the middle of the past decade and recently peaked at 80% of GDP - more than double the level of 60 years ago.

Despite the seemingly large amount of cash held by US corporations, their debts far outweigh the balance in their collective bank account. According to the most recent Flow of Funds report published by the Federal Reserve, US corporations have approximately $7.3 trillion in outstanding debt; the oft-quoted $2 trillion of cash sitting on corporate balance sheets pales by comparison. If borrowing costs were to rise, corporations would need every dollar of their available cash to keep from going under.

Another key factor that is under reported in the "cash on the sidelines" story is that up to $1 trillion of the cash held by US companies sits outside American borders, where it is essentially unavailable to fund US operations. While vast amounts of capital can move across international borders with just a few keystrokes, the repatriation of cash generated by US international subsidiaries could result in a huge tax liability. The balances reported in the press do not take into account these taxes. As a result, the amounts quoted by the press are overstated. But even if we ignore the impact of taxation, and simply assume that all cash is available to pay down debts, American businesses still owe far more in debt than the cash they have on hand.

The death blow to US corporations could come when US interest rates rise to historically normal levels. A four-percentage-point rise in the interest rates paid on debt by US corporations would cost them nearly $300 billion per year in additional interest costs. That amounts to 17% of corporate profits for all of 2010. When faced with rising interest costs that cut into profits, companies will likely look to cut expenses in all areas, including labor. This could start a vicious cycle of corporate cutbacks, declining household income, reduced aggregate demand, and slowing production, which would start the cycle all over again.

In short, despite huge amounts of cash on their balance sheets, America's largest companies are as broke as the rest of the country, and not only are they in no position to hire workers, but higher interest rates could result in more layoffs at a time when the nation can least afford it. Given these factors, economists, journalists and politicians should be applauding corporate cash reserves not deriding them. Given that a real recovery will not come until America as a country has paid down some of its debt, we should not be urging our corporations to throw caution to the wind.

For full access to the remaining articles in The Euro Pacific Global Investor Newsletter, please click here to subscribe.

Subscribe to Euro Pacific's Weekly Digest: Receive all commentaries by Peter Schiff, John Browne, and other Euro Pacific commentators delivered to your inbox every Monday!

For a great primer on economics, be sure to pick up a copy of Peter Schiff's hit economic parable, How an Economy Grows and Why It Crashes

Neeraj Chaudhary is an Investment Consultant in the Los Angeles branch of Euro Pacific Capital. He shares Peter Schiff's views on the US dollar, the importance of the gold standard, and the rise of Asia as an economic power. He holds a B.A. in Economics from the University of California at Berkeley.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.