U.S. Consumers Have Big Banks To Blame For High Gasoline Prices

Commodities / Gas - Petrol Apr 02, 2011 - 05:58 AM GMTBy: Dian_L_Chu

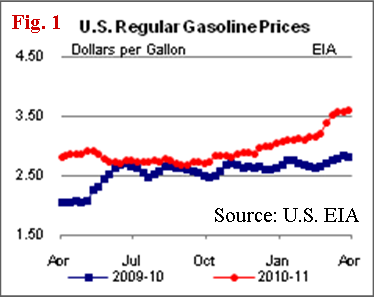

There is a bit of irony here in that the very same banks that taxpayers bailed out, and saved from going completely belly up, are now making you pay once again in the form of higher Oil prices, and the resultant higher gasoline prices at the pump (Fig. 1). Don`t be fooled by the rhetoric generated in the media by the Big Banks regarding the Middle East.

There is a bit of irony here in that the very same banks that taxpayers bailed out, and saved from going completely belly up, are now making you pay once again in the form of higher Oil prices, and the resultant higher gasoline prices at the pump (Fig. 1). Don`t be fooled by the rhetoric generated in the media by the Big Banks regarding the Middle East.

It All Started With Jackson Hole….

This run-up in oil prices started with Fed Chairman Bernanke`s Jackson Hole speech where the big banks realized they were going to get a bunch more juice in the form of POMO operations by the Federal Reserve to play around in markets with.

And what did the large financial institutions do with this newly created juice? Instead of allocating the almost zero percent money they are all borrowing to productive activities such as lending loans to small businesses which will create jobs and stimulate the economy, the big banks have decided that since the fed is electronically printing money and providing extra liquidity/juice for financial markets that this is inflationary and devalues the dollar.

All Fed Juice Leads to Commodities

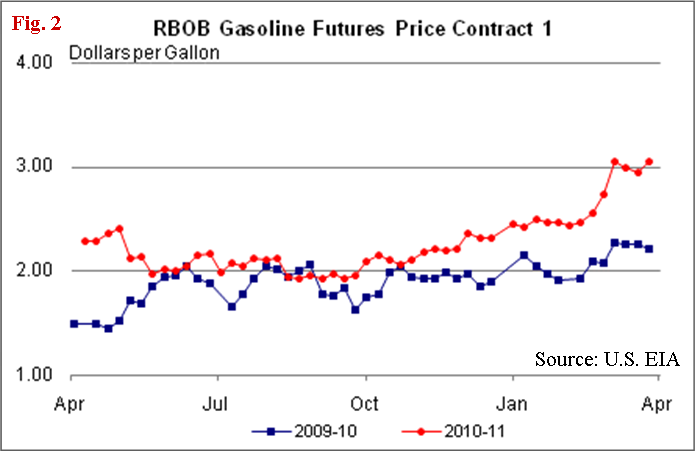

And just to make things worse, the big banks have decided to take their cheap capital they borrow at basically zero percent , and invest into commodities, i.e., agricultural futures like Wheat, Corn, and Soybeans, energy futures like Oil and Gasoline (Fig. 2), and industrial and precious metals like Copper, Gold and Silver.

The unique aspect is that loose monetary policy isn`t problematic at face value when you are trying to stimulate growth, it is what the Big Banks are utilizing this cheap capital for that becomes problematic from an inflation standpoint. The very problem that the Banks are worried about in regards to inflation, they are in fact responsible for creating through self-fulfilling investment practices with regard to this cheap capital at their disposal.

Long Commodities, Short Dollar - Adding Inflation

But it gets worse because at the same time they also short the US Dollar, and going long the commodity currencies like the Canadian and Australian Dollar, which further exacerbates the slide in the US Dollar (Fig. 3), reinforcing the entire trade that they need to buy more commodities as an inflation hedge, further juicing up commodities like oil and gasoline.

Inflation Up, Purchasing Power Down

The consumer is hurt in two ways. First is that higher prices eat into their monthly budget with a higher percentage of their disposable income needed for purchasing items like milk, eggs, bread, and gasoline. Secondly, because the Dollar is losing its store of value, the consumer is losing their purchasing power, i.e., what a dollar is worth in relative terms around the world, and what it can buy. In other words, it is

like getting a pay cut at work from your company, the amount hasn`t changed, but what goods that amount will be able to buy is less.

Consumers Getting Double Stiffed

The Big Banks like JPMorgan Chase, Goldman Sachs, Morgan Stanley, HSBC, UBS, and BOA-Merrill Lynch are some of the largest energy traders in the world. They all derive considerable trading revenue from the markets each quarter. So when you hear that Goldman Sachs, or BOA didn`t have a single losing trading day for a given quarter, these banks are taking a lot of money out of the market, and much of their hefty trading profits are generated from commodities like food and energy.

And guess who is footing the bill for these trading profits? Yes, the US consumer, the very same US consumer who bailed them out during the financial crisis. Talk about getting short shrifted twice. (I cleaned up the last sentence, but you get the gist.)

2008 Oil Bubble Redux

Currently, there are no supply shortages in the oil market, but what you have is a bunch of speculators going wild pushing up energy prices hyping the Middle East, Peak Oil, The Nigeria Card (remember in 2008 where every little Nigerian pipeline was under attack every day during that run-up, and all the sudden Nigerian pipeline attacks were inconsequential for two years—that`s the Nigerian Card-bring it out when traders are in Trend Trading Nirvana.)

What we have here is a 2008 redux. The Brent contract on the ICE exchange is being used to engineer prices up, as it is an unregulated exchange with no real transparency on position limits by the Big Banks. The Big Banks are also piling a bunch of money into commodity related ETF`s and mutual funds, which in turn have to buy exposure to the futures market in all these commodities. Add in the hedge funds, pension funds, money managers, and retail traders, and voila! you have these bubbles created which have no relation to the underlying fundamentals.

Trend Trading Hyper Leverage

It all comes down to fund flows, capital going into the commodity trade because it is going up, further adding fuel to fire that this is the place to be-- Welcome to the self-reinforcing cycle of Trend Trading.

However, it gets even worse, because we have one-sided markets with no substantial pullbacks which normal healthy markets have. The Big Banks are able to add to their original positions with the profits they have locked in with stops that are already hugely profitable. The Big Banks are then buying additional futures contracts, pushing these same commodities up further, until eventually the bubble bursts like 2008, when everyone runs for the exits at the same time.

The effect is that by adding to original positions via locked in profits, the Big Banks have added even more liquidity/juice to the market – a form of hyper leverage without real risk. This results in the consumer paying more at the pump, not because there is less supply of oil in the market, but largely because of a trading technique that artificially inflates prices by adding more juice to the equation.

Crude Oil – An 'Engineered' Market

I know we had a recession, but Crude Oil went from $143 dollars a barrel to $33 in six months. Now, you don`t think demand dropped off that much, do you? It didn`t, even when a consumer lost their job , which at most we went from a 5% unemployment level to slightly above 10%--did this 5% completely stop consuming fuel? I know this is an oversimplification; however you can follow where I am going with this line of reasoning-- Crude Oil should never have been $143 a barrel in the first place!

It was stage-managed to those levels the last time by the Big Banks like Goldman Sachs. Remember the infamous “$200 Oil Call” by the Goldman analyst – do you truly believe that happened by accident? It served a purpose for Goldman Sachs at the time, to help ‘market’ the price of Crude Oil.

Banks Long Oil...Gee, You Think?

You now have Nomura Securities with their $220 Oil Call, and J.P. Morgan pumping out weekly analysts forecasts regarding Crude Oil targets of $130 for the second quarter. Why make these price forecasts available to the media and the public if they aren`t used for a purpose? Wouldn`t they want to keep these reserved for their paying, private clients? Gee, I wonder if they are positioned long in the Oil Market?

You guessed it. The same Banks that won`t give you a loan, or a credit card because your credit score isn`t perfect is making your financial condition even worse by pushing up the price of Oil, Food and Gasoline when there are no real supply shortages in the market. What is taking place in the market are traders hitting revenue goals by trading commodities in order to maximize their bonuses.

Fed, The Enabler

This is not all the Big Banks fault, as just like in 2005-2007, regulations were eased to let them all lever up over 40 times base capital. Well, Chairman Bernanke and the Fed`s extremely loose monetary policies have enabled the banks to profit enormously from trading behavior and investment choices which inevitably have lead to the creation of another inflationary bubble. We still have a long way to go in recovering from the last Fed fueled bubble regarding the Housing Industry from the Alan Greenspan era of overly loose monetary policy.

Higher Margin Requirement, The Unwilling Accomplice

In addition, the CFTC was supposed to come up with position limits for the Big Banks over 3 months ago, but even the limits they were considering were not going to do any good. The CME has raised margin requirements on all the commodities, but this actually makes things worse because it squeezes out more of the smaller speculators. It concentrates more of the contract from a percentage standpoint with the Big Banks who have access to all the capital they could ever need at zero percent interest.

If you raise margins for the Big Banks, they just go borrow more money to cover the raised requirements, but they never have to reduce positions like the smaller players. This makes for less of a diverse market. Therefore, raising margins isn`t the answer either. In other word, don`t expect any relief from the CFTC or the exchanges--they really are powerless to reduce this type of speculative fervor.

Two Ways to Skin Big Bank Cats

There really are only two options:

1) Bernanke has to immediately change his tone, and become much more hawkish regarding inflation, and he needs to do this immediately, as in, Monday morning. He needs to say something to the effect: “Due to rapidly building food and energy cost pressures, the fed needs to seriously discuss the idea of cutting short QE2 at our next monetary policy meeting on the 27th of April”.

That`s literally all Bernanke would have to say, not that they are going to cut QE2 short, just discuss the idea, and that you are worried about rising inflationary pressures in the economy exemplified by the unprecedented spike in gasoline prices. This would send the right message to the speculators, and curb much of the speculative fervor. All commodities would instantly sell off. For example, Oil would drop by $3.50 in an hour, and the RBOB contract would drop 18 cents.

This is how you can even maintain all the benefits of a relatively loose monetary policy without all of the acute negative consequences of unchecked speculation, which we are experiencing right now in commodities. It’s a one sided trade, that is crowded, unnatural, and bad for markets and consumers alike.

2) The second option is more micro managing an individual commodity. Let`s take Oil for example. President Obama could make a statement on Monday morning stating the following: “I have decided to open up the Strategic Petroleum Reserves to the market, not because there are any supply shortages in Crude Oil, far from it, actually, but we want to target the excessive speculation that we believe is occurring right now in the Oil market”.

Again that`s all it would take and Crude Oil would be down $3.50 and gasoline would drop as well. You do not even need to sell any Oil from the reserves, it actually isn`t needed, but the important part is the message that you are sending to markets, “this is not a riskless, one way trade.”

Fed's Punchbowl Ends Here & Now

Speculation isn`t always bad, in fact, it often serves many valid purposes within markets. But excessive speculation to the point where markets diverge considerably from the underlying fundamentals is never a good thing. And it is important for those in positions of authority to manage such markets appropriately through legislative regulation, monetary policy, or simply managing market participants’ expectations by sending the right types of messages to markets.

However, our policy makers so far have mismanaged the message being sent to Wall Street. It is something along the lines of “Get drunk at the Fed inspired liquidity punchbowl, and don`t worry about the mess you make”. The message the Federal Reserve should be sending is, “Make sure you don`t drink too much at the liquidity punchbowl, or we will take it away”.

The reasoning here is that it is always much easier to prevent the mess in the first place, than to try and clean it up afterwards. We have reached the point where the Fed needs to take the punchbowl away!

Dian L. Chu, M.B.A., C.P.M. and Chartered Economist, is a market analyst and financial writer regularly contributing to Seeking Alpha, Zero Hedge, and other major investment websites. Ms. Chu has been syndicated to Reuters, USA Today, NPR, and BusinessWeek. She blogs at http://www.econmatters.com/.

© 2011 Copyright Dian L. Chu - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.