Will the Mid-Term U.S. Elections Drive the Stock Market Into High Gear?

Stock-Markets / Stock Markets 2010 Sep 27, 2010 - 07:30 AM GMTBy: Money_Morning

Jon D. Markman writes:

The past five days added more hues to the emerging snapshot of U.S. economic growth that is sluggish and top-heavy, but still rolling forward -- kind of like a tank that can't get out of first gear. New data shows that U.S. GDP is back to 70% of its pre-recession strength, but jobs have recovered only 9%. It's this disconnect between output and employment that has made the current "recovery" seem so anemic.

Jon D. Markman writes:

The past five days added more hues to the emerging snapshot of U.S. economic growth that is sluggish and top-heavy, but still rolling forward -- kind of like a tank that can't get out of first gear. New data shows that U.S. GDP is back to 70% of its pre-recession strength, but jobs have recovered only 9%. It's this disconnect between output and employment that has made the current "recovery" seem so anemic.

That was fine for investors, who bid up risky assets in the past week just as they had the previous three weeks. The S&P 500 rose 2%, the Nasdaq 100 rose 3.5%, overseas large caps rose 3.3%, and emerging markets rose 2.5%. Gold rose 1.7%, silver rose 3%, crude oil rose 2.1%, and even bonds rose 1.5%. Among the overseas markets we care most about, ishares MSCI Thailand Index Fund (NYSE: THD) rose 5.6%, Wisdom Tree India Earnings Fund (NYSE: EPI) rose 3.3%, and ishares MSCI Singapore Index Fund (NYSE: EWS) rose 2.4%.

Equities have pursued the upward path for the best of reasons, and to the bears the most enervating: Companies with irregular fiscal years have been reporting summer-quarter earnings that have mostly beat expectations -- plain and simple. And not small, goofy companies either. We're talking about retail and software giants Best Buy Co., Inc. (NYSE BBY) and Oracle Corp. (NASDAQ: ORCL), and even the humbled one-time leader of the wireless handset world, Research in Motion Ltd. (NASDAQ: RIMM).

The second half of September is the part that has given the month its bad reputation, so bulls are not out of the woods yet, so to speak. In fact, probabilities favor a lot more volatility ahead. But as I mentioned last week, when the market has cruised above its 10-, 50- and 200-day averages by the middle of September of a mid-term election year of a first-term president it has a strong tendency to keep speeding right into the end of the year and beyond.

Mid-term elections matter for market performance for two reasons: It's a time when an effective president can bend the government bureaucracy to the task of producing the best possible spin on economic data. And it is also a time when backers of the party out of favor are energized by hopes that it can make strides in Congress and thus aid its Wall Street backers.

When the market is already in a sour state coming into this period, the political anxieties fuel the despair on both sides. When the market is rising into this period, both sides begin to dream a little. We're in the latter case now, so if you look at political and financial commentary you will see both sides of the political spectrum claiming that they have their opponents just where they want them.

Getting down to the numbers, here's how it has worked out:

-- Looking at all mid-Septembers before mid-term elections since 1902, the broad market tends to rise over the next 10 weeks by 3.5%, with a 16 of 20 win/loss ratio. And the positive periods are +6.8%, vs. negatives (including 1930) at -9.8%.

-- Looking just at mid-Septembers of mid-term years when the market is above its 10-, 50- and 200-day averages, the win/loss ratio is 5 out of 6, with an average gain of 5.3% over just four weeks, and an average of +7% in the positive results and only -2.7% in the negatives. Some of the best were 1982, 1958, 1954 and 1950.

So get out your Reagan, Truman and Eisenhower memorabilia and let's hope the next few months run just like they did in the times of ''Give 'Em Hell Harry,'' "I Like Ike" and "Morning in America." And just to belabor the point a little, you should know that the one losing month in the second case was 1994, and the rally just took a little longer getting going, because 1995 was a barn-burner.

Now as for the broader perspective, stocks are actually looking much better than most people think. If you asked the man or woman in the street whether the U.S. stock market was up or down this year, I think they would guess down. But the reality is that larger American companies are now positive for the year, with the S&P 500 up almost 3%, while the small-caps are up 7% and mid-caps are up 10%.

Moreover if you take out the big banks and energy stocks, which continue to wallow, the industrial companies in the United States, which are in the Industrials SPDR ETF (NYSE: XLI), are actually up 15%. And if you look overseas, as you know, then the picture is even brighter, with emerging markets Thailand and ishares MSCI Chile Investors Index Fund (NYSE: ECH) are up 37% and 34% for all the reasons we have detailed.

Keep in mind we are now entering the last phase of the part of the calendar that tends to give investors trouble, and heading toward the best time of year, which is mid-October to mid-April. The goal of investors who pay attention to cycles and the calendar is to buy between now and the end of October and hold for six to seven months.

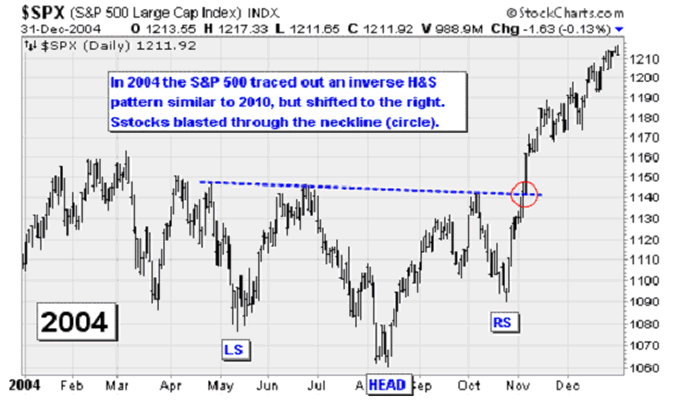

You can see how an inverse head-and-shoulders pattern similar to the current one played out in 2004 in the chart above. When stocks got to that neckline (circle) the expectation was for it to fail -- but it blasted through. That would be the most unexpected result now, so you can categorize it as a distinct possibility.

The bottom line is that any weakness that emerges in the coming week or two should be bought, and if there is no weakness then we should buy breakouts because stocks are cheap if most companies have managed through the recent weakness in spending as well as Oracle and Best Buy.

MORE POSITIVES FOR CONTRARIANS

It's hard to determine what constitutes a contrarian anymore.

My bearish associates contend they are the contrarians because everyone they see on TV appears to be chirpy now that the market has been up two weeks in a row. They are never happier than when they see more bullish remarks in the media, because it makes them feel like outlaw outliers.

My bullish associates contend they are the contrarians because the outflows from equities accelerated recently, and overall sentiment is lousy despite the move higher this month. They contend that "no one is in the market," and argue that if stocks make a jailbreak higher in coming weeks then there will be a mad rush from the sidelines as people succumb to a different sort of fear -- the one that arises from missing out from a chance to make money in stocks.

I try to stay out of this debate because it is kind of pointless. I'm bullish on fast-growing companies that are cheap and going up, and I'm bearish on companies that are expensive and flat-lining or going down. I've never been one of those pure ''deep-value'' people or a pure momentum guy. Here at Strategic Advantage we are right in between -- pragmatic opportunists who study the odds, run the numbers, and roam the world for chances to win big over multi-month time frames.

It's in that context that I want to talk about some more of the data compiled by British money management firm Collins Stewart in a presentation that I saw recently.

-- Non-farm payrolls have a correlation of 0.92 to temporary employment pushed ahead by four months. That means the two data series are highly correlated, which in simpler language means that when one happens the other virtually always happens. For the past four months, temp employment has shot straight up. That probably means companies are going to start hiring full-timers too. Maybe won't have a "jobless recovery" after all. That would shock people.

-- Debt-financed consumption -- which is basically 'consumer credit + home equity loan growth less retail sales growth -- has started to rise again. This suggests that household deleveraging may be just about over. That should be good for retailers like Best Buy, American EagleOutfitters (NYSE: AEO) and Nordstrom Inc. (NYSE: JWN).

-- Consumers' and businesses' balance sheets have improved to the point where banks are more willing to lend to them again. Data shows that loan growth is finally becoming "less worse," which is the first step toward getting better.

-- In periods following recessions, analysts who feel they were inappropriately optimistic in the prior bull market become excessively pessimistic by up to 20% after a bear market concludes. Estimates are always way too high in the latter half of bull markets and the first half of bear markets, while they are always way too low during the first three quarters of bull markets. At present, corporate profits are actually rising faster than in the last six expansions, according to Zacks Investment Research data, but estimates are low -- so that provides an opportunity for upside surprises.

-- The reason we care about earnings is that there is a positive long-term correlation between the stock market and operating earnings. As long as the slope of earnings is rising, the S&P 500 has always risen too. And when things go nutty on the upside, like the span of 1996-2000, the market gets way out in front of earnings growth.

-- Now since EPS estimates are probably too low vs. the way earnings will actually come in, valuations are probably too low -- trading at only 12x expected 2011 earnings. This is really important: Price/earnings multiples are normally very tightly correlated to interest rates and the core rate of inflation. When rates and inflation are low (0.25% and 1.5% now), P/Es tend to inflate.

According to the Collins Stewart study, the correlation suggests that P/Es should be as high as 20x right now -- and are probably on that path. Currently 2011 and 2012 consensus estimates for the S&P 500 are $96 and $108, respectively. You can do the math yourself, but the bottom line is that if confidence reverts to normal levels, the 2007-2009 bear market could be fully reversed next year.

PAST WEEK IN THE ECONOMY

Now here is our special weekly look at the major measurements of the economy, with a big hand from the analysts at Econoday.

-- Housing starts showed unexpected strength in August, with starts jumping 10.5% after rising just 0.4% in July. The annualized pace was much faster than expected, at 598,000 units, vs. 550,000. Starts are now up 2.2% over the past year, which is fairly surprising.

-- Building permits improved, rising 1.8%, after falling 4.1% in July. The biggest gain was in multifamily dwellings, which rebounded 9.8%. Single-family permits fell 1.2%.

-- Home-builders are pessimistic, as they see traffic through model homes slipping. Don't expect any improvement in single-family home construction in September.

-- Bottom line for housing is that construction workers are back to work building apartment houses, but builders that specialize in single-family homes will remain under pressure.

-- Existing home sales bounced back a bit, rising 7.6% in August to a 4.13 million units per year rate, up a lot from the 3.84 million rate of July. All regions benefited. Supply of existing homes declined to 11.6 months' inventory, down from 12.5 months in July. This is still a very high level and is keeping pressure on home prices. Best subgroup was existing condos and co-ops, up 8.5%.

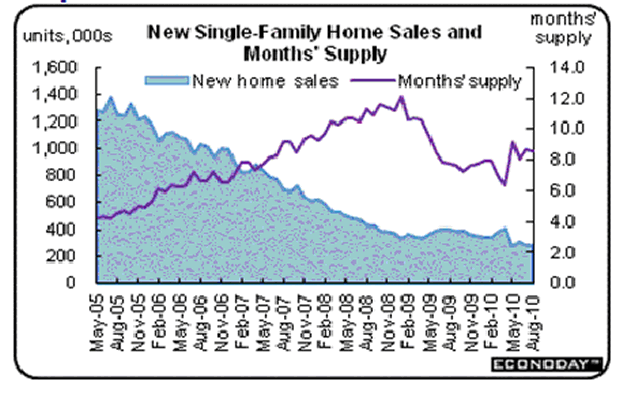

-- New home sales made no improvement, as they were unchanged in August from July or even May for that matter. Supply is high and wearing down prices, which ticked lower again in August by 0.6% to a median of $204,700, a seven-year low. An index of federally financed homes' prices is now down 3.3% for the past year, vs. -2.6% in July.

-- Durable goods orders slipped 1.3% in August after a 0.7% rebound in July, but the underlying momentum is still positive. Excluding transportation (vehicles, trains and airplanes), new durables orders rose 2%, rebounding from a 2.8% drop in July. All non-transport areas were good, including fabricated metals up 1%, machinery +3.9%; computers and electronics, +3.8%.

-- The Great Recession was declared to have concluded in June 2009, after starting in December 2007. So the recession lasted 18 months, which means it was the longest since the end of World War 2. Now you can see why I have refused to use the term "double dip." Any new decline in output would constitute a brand-new recession, and not a second leg of the last one.

-- Index of Leading Indicators advanced 0.3% in August, after a 0.1% rise in July. This suggests that no new recession is imminent. Best components were the interest rate spread (T bonds less the Fed Funds rate), a rise in the money supply and an increase in the factory work week, consumer expectations and factory orders.

-- Federal Reserve announced on Tuesday it was ready to loosen credit further through its quantitative easing techniques as it believes "the pace of recovery in output andemployment hasslowed in recent months." It also changed its focus to disinflation or deflation, from inflation -- a huge development.

-- Bottom line for the week: manufacturing has retained its strength but housing remains in the dumps. Since the Fed wants to jump-start jobs as much as possible, it plans to double down on its efforts to help businesses borrow the funds they need to expand production and employment.

WEEK AHEAD FOR THE ECONOMY

Monday: Nothing major scheduled. Earnings: Paychex Inc. (NASDAQ: PAYX). Zale Corp. (NYSE: ZLC).

Tuesday: Conference Board's consumer confidence index. Earnings: Walgreens Co. (NYSE: WAG).

Wednesday: Nothing major scheduled. Earnings: Actuant Corp. (NYSE: ATU), Family Dollar Stores Inc. (NYSE: FDO), Xyratex (NASDAQ: XRTX), Worthington Industries Inc. (NYSE: WOR).

Thursday: GDP growth for the second quarter will be re-estimated. Initial jobless claims for the prior week will be announced. Earnings: Accenture plc (NYSE: ACN), Charles River Laboratories (NYSE: CRL), McCormick & Co. (NYSE: MCK).

Friday: Sales of domestic light motor vehicles (probably down). Personal income for August (probably slightly up). Reuters/Univ of Mich. Consumer sentiment survey (probably down). ISM manufacturing composite index (down slightly). Construction spending (probably up a touch).

[Editor's Note: Money Morning Contributing Writer Jon D. Markman has a unique view of both the world economy and the global financial markets. With uncertainty the watchword and volatility the norm in today's markets, low-risk/high-profit investments will be tougher than ever to find.

It will take a seasoned guide to uncover those opportunities.

Markman is that guide.

In the face of what's been the toughest market for investors since the Great Depression, it's time to sweep away the uncertainty and eradicate the worry. That's why investors subscribe to Markman's Strategic Advantage newsletter every week: He can see opportunity when other investors are blinded by worry.

Subscribe to Strategic Advantage and hire Markman to be your guide. For more information, please click here.]

Source : http://moneymorning.com/2010/09/27/stock-markets-3/

Money Morning/The Money Map Report

©2010 Monument Street Publishing. All Rights Reserved. Protected by copyright laws of the United States and international treaties. Any reproduction, copying, or redistribution (electronic or otherwise, including on the world wide web), of content from this website, in whole or in part, is strictly prohibited without the express written permission of Monument Street Publishing. 105 West Monument Street, Baltimore MD 21201, Email: customerservice@moneymorning.com

Disclaimer: Nothing published by Money Morning should be considered personalized investment advice. Although our employees may answer your general customer service questions, they are not licensed under securities laws to address your particular investment situation. No communication by our employees to you should be deemed as personalized investent advice. We expressly forbid our writers from having a financial interest in any security recommended to our readers. All of our employees and agents must wait 24 hours after on-line publication, or 72 hours after the mailing of printed-only publication prior to following an initial recommendation. Any investments recommended by Money Morning should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company.

Money Morning Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.