Eight Financial Fault Lines Appear In The Euro Experiment!

Currencies / Euro Feb 18, 2010 - 05:12 AM GMTBy: Gordon_T_Long

Tremors were heard across Europe and around the world last week. There was little mistaking the clear fracturing sounds of the European Monetary Union.

Tremors were heard across Europe and around the world last week. There was little mistaking the clear fracturing sounds of the European Monetary Union.

Receiving less fanfare than the political hyperbole of EU solidarity, was surfacing evidence of serious fissures that exposed similar financial schemes which took the US to the financial abyss.

Our research has identified eight fault lines now visible in the Euro experiment. Each is serious. As a combination they have the potential to be devastating. They are all now fully in play.

|

|

FAULT LINE #1: CURRENCY SWAPS

Greek accounting ‘irregularities’ that have resulted in massive distortions of Greece’s actual fiscal imbalances was not the news last week. Manipulated Greek government bookkeeping has been known for some time. What sorcery the Greek government had magically mixed in its hidden brew to accomplish the irregularities however began receiving much higher levels of media attention after the Feb. 1 release of their report commissioned by the Finance Minister in Athens.

Currency Swaps it turns out were what the great Merlin – Goldman Sachs had recommended and sold to the hapless Greek politicians with which to hide their spendthrift ways. Goldman Sachs was not initially identified in the Feb 1st report. (1)

Suspicious eye brows were quickly raised when Greece’s Finance Minister responded to the new details reported by Reuters:

"The kind of derivatives contracts reported by some newspapers were legal at that time, Greece was not the only country to use them...

They were made illegal, [and] we have not used them since then."

The obvious questions that alarmed investors:

WHO ARE THE OTHER COUNTRIES HE IS REFERRING TO? - HOW BROAD BASED WAS IT?

ARE THEY STILL USING THEM BUT IN DIFFERENT HYBRID FORMS?

It also begged the question of overall supervision of accounting that the EU statistical agency exerts? How transparent are the EU sovereign country books? There are a lot of questions that will be asked of Greece and other countries over the next few weeks. As my grandmother wisely advised me - “There is never only one cockroach!”

FAULT LINE #2: SPC & PPI / PFI

Delving into the details as the breaking news on Greece unfolded; I was reminded of my research during the early stages of the Enron scandal. At that time I started discovering the world of SPE’s (Special Purpose Entities) that until that time were almost unheard of, but it turned out were being slyly and extensively employed. I remember Enron CFO Andrew Fastow defending his extensive use of such vehicles by referring to the fact GE had over 2400. I was also reminded of the early stages of the financial crisis when I learned about banks using SIV’s (Structured Investment Vehicles) to sell CDOs and protect themselves with CDS’s – all new instruments and somehow never visible to the light of day. The experience taught me that in today’s wild west of global financial gamesmanship to always dig deeper – and fast!

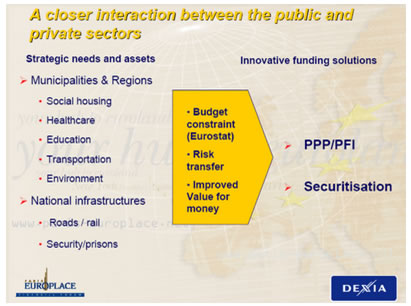

Last week I discovered SPC’s (Special Purpose Company) & PPI / PFI’s. Not familiar with them? You had better be because they will soon likely be cocktail party chatter. These are financial instruments and arrangements that allow governments to factor ‘receivables’ and thereby camouflage debt. They are being broadly employed as the standard marketing slide below would indicate.

Public Private Partnership – PPI: An umbrella term for Government schemes involving the private business sector in public sector projects.

Public Private Partnership – PPI: An umbrella term for Government schemes involving the private business sector in public sector projects.

Private Finance Initiative – PFI: a form of PPP developed by the Government in which the public and private sectors join to design, build or refurbish, finance and operate (DBFO) new or improved facilities and services to the general public. Under the most common form of PFI, a private sector provider will, through a Special Purpose Company (SPC), hold a DBFO contract for facilities such as hospitals, schools, and roads according to specifications provided by public sector departments.

Over a typical period of 25-30 years, the private sector provider is paid an agreed monthly (or unitary) fee by the relevant public body (such as a Local Council or a Health Trust) for the use of the asset(s), which at that time is owned by the PFI provider. This and other income enables the repayment of the senior debt over the concession length. (Senior debt is the major source of funding, typically 90% of the required capital, provided by banks or bond finance). Asset ownership usually returns to the public body at the end of the concession. In this manner, improvements to public services can be made without upfront public sector funds; and while under contract, the risks associated with such huge capital commitments are shared between parties, allocated appropriately to those best able to manage each one (2).

Edward Hugh at Credit Writedowns does a first rate job of laying out how all this works and where the looming exposures are hidden in his February 14th article: Just what is the real level of government debt in Europe? He concludes:

a) They assume a certain level of headline GDP growth to furnish revenue growth to the public agencies committed to making the payments. Following the crisis these previous levels of assumed growth are now unlikely to be realized.

b) They assume growing workforces and working age populations, but both these, as we know, are now likely to start declining in many European countries.

c) They assume unchanging dependency ratios between active and dependent populations, but these assumptions, as we also already know, are no longer valid, as our population pyramids steadily invert.

Given all this, a very real danger exists that what were previously considered as obscure securitisation instruments, so obscure that few politicians really understood their implications, and few citizens actually knew of their existence, can suddenly find themselves converted into little better than a glorified Ponzi scheme.

And if you want one very concrete example of how unsustainable debt accumulation can lead to problems, you could try reading this report in the Spanish newspaper La Verdad (Spanish, but Google translate if you are interested), where they recount the problems being faced by many Spanish local authorities who are now running out of money, in this case it the village of San Javier they have until the 24 February to pay a debt of 350,000 euros, or the electricity will simply be cut off! The article also details how many other municipalities are having increasing difficulty in paying their employees. And this is just in one region (Murcia), but the problem is much more general, as Spain’s heavily over-indebted local authorities and autonomous communities steadily grind to a halt.

FAULT LINE #3: TITLOS PLC (SPV)

But it gets worse, unfortunately much worse!

But it gets worse, unfortunately much worse!

TITLOS PLC (SPV) may be to Greece what ‘RAPTOR’ was to Enron. TITLOS PLC (SPV) may be the real smoking gun in the Greek crisis and unfolding Euro Crisis.

Tyler Durden and Marla Singer at Zero Hedge have done a masterful job of investigation and outlining the murky relationship between the rating agencies and the rating of the underwritten swap agreement securitization SPV called Titlos PLC. All brought to you by Goldman Sachs.

As I mentioned earlier, I feel like I’ve seen this play before. The script is right out of the pages of Enron and the US Sub-Prime debacle! It even has the same supporting cast member: Goldman Sachs!

Durden and Singer’s Feb 15th article is entitled: Is Titlos PLC (Special Purpose Vehicle) The Downgrade Catalyst Trigger Which Will Destroy Greece? It is extensive with supporting Scribd documents of documentation that has now mysteriously been removed from public viewing by Greek officials.

Their conclusions:

On December 23, 2009, Moody's downgraded Titlos, following the prior day's downgrade of Greece itself from A1 to A2 with a negative outlook.

Fact: last week Moody's said it could further downgrade Greece to Baa1.

Fact: the Titlos PLC rating mirrors that of Greece itself.

Fact: according to Moody's "Framework for De-Linking Hedge Counterparty Risks from Global Structured Finance

Cashflow Transactions Moody's Methodology" a counterparty can enter into a hedge transaction with an SPV and continue to participate in that transaction without collateralizing its obligations so long as it maintains a long-term senior unsecured rating of at least A2.

When (not if) Titlos is downgraded again, and its rating drops below the A2 collateralization threshold, look for AIG's margin call driven liquidity crisis escalation from the fall of 2008 to spread to Greece. And that's not all.

The Titlos SPV itself may be null and void should the rating of the National Bank of Greece, as the Hedge Provider, drop below a "relevant rating" as defined in the hedge agreement. Should Greece then be forced, at Titlos' option, to unwind the swap agreement, and be forced to cash out to the tune of €5.4 billion (net of the 107.54 issuance price), look for all hell to break loose.

Greece has suddenly found itself at the mercy of a Moody's, whose just one additional notch down, would increase the funding needs by almost 40% in addition to near term maturity requirements. Score yet one more for the off-balance sheet securitization puzzle, so prevalent in our day and age, courtesy of Wall Street's "innovation" masters - Goldman Sachs.

Do you have the stomach to go on?

FAULT LINE #4: GREEK CDS’s

The Wall Street Journal reports:

Germany's willingness to consider a rescue may also reflect the exposure of the country's own banks to the vulnerable countries.

German banks are major lenders in Greece, for example, collectively carrying about $43 billion in Greek debt on their books, including loans to private individuals and companies, according to Bank for International Settlements data for the third quarter of 2009. Among EU countries, only France's banks, with $75 billion, carry a larger share of Greece's $303 billion in debt to foreign banks.

In addition, some of Germany's public-sector banks, known as Landesbanken, have issued insurance-like contracts on Greek debt, known as credit default swaps. The total exposure of the country's eight Landesbanken is unclear.

Two of the banks, Bayern LB and West LB, described their exposure to Greek credit default swaps as negligible. Hanover-based NordLB and LBBW in Stuttgart declined to comment. Frankfurt-based Helaba and HSH Nordbank in Hamburg didn't immediately respond to requests for comment. SaarLB, in Saarbrücken, couldn't immediately be reached.

Credit Writedown reports on the CDS exposure of the German Landesbanks to Greece:

If Greece were to default, the Landesbanks, which have already lost tens of billions, would be on the hook for even more. Clearly, the German government is aware of this situation and this is certainly a major part of their political calculus.

The real driver here is not that the private debt problem is becoming a sovereign debt problem, but the opposite–the sovereign debt problem is threatening to renew the private sector banking crisis. Consider the BIS data that is cited in press reports today: German bank exposure to Greece is 43 bln euros, to Portugal 47 bln euros, to Ireland 193 bln euros and to Spain 240 bln euros.

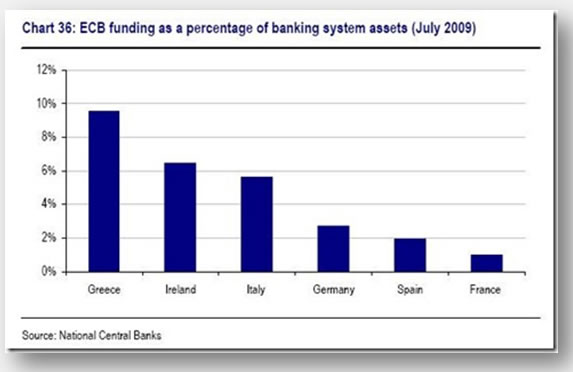

FAULT LINE #5: REPO ARRANGEMENT

The FT Alphaville reported on December 8th in How do you say vicious circle in Greek?:

The interesting bit is that the Greek banks don’t seem to have an immediate funding crisis on their hands since the lion’s share of liabilities come from their deposit base. UBS analysts speculate that the banks are merely using the ECB to receive low cost funding with Greek sovereign debt assets as collateral. That makes the Greek sovereign debt crisis a Greek bank crisis then – as this funding source may disappear with sovereign credit downgrades.

Now, if you were a Greek resident, you have to feel a bit panicky about the safety of your hard-earned savings given this scenario (see Guardian article). So, we could easily see the sovereign debt crisis spill over into bank runs. And if Greek banks implode, there is going to be a knock-on effect for other weak banking sectors like the Austrian or Irish. This is how contagion works.

Let’s not forget that Greek banks do have some funding needs. How are they going to roll over repo debt if the sovereign is having trouble?

Rumors are starting that counterparties are not rolling over repo arrangements; this is exactly how Bear Stearns failed

FAULT LINE #6: GREECE & THE BALKANS

Credit Writedown reports the following:

Another fault line lies in the connection between Greece and the Balkans, where Greek banks are very active. For example, around the time that the Bear Stearns crisis was brewing in March 2008, the internet site Global Politician reported the following (3):

According to the Greek newspaper, Elefteros Topos, between the years 2000-2006, Greeks invested almost 263 million USD in their nascent neighbor. That would make Greece the second largest foreign investor in Macedonia. Of the 20 most sizable investments in Macedonia’s economy, 17 are financed with Greek capital. More than 20,000 people are employed in Greek-owned enterprises (c. 6% of the active workforce in this unemployment-plagued polity).

Greeks are everywhere: banking (28% of their total investment in the country); energy (25%); telecommunications (17%); industry (15%); and food (10%).

The foundations of the current presence of Greece in all Balkan countries – including EU members, Romania and Bulgaria – were laid in the decade of the 1990s.

The Greeks banks are heavily exposed in the Balkans and elsewhere in Eastern Europe. But, as I said in a previous post, Greek banks are using the ECB for low cost funding – with Greek sovereign debt as collateral. Therefore, a Greek sovereign debt crisis could impair the liquidity of Greek banks and therefore have knock-on effects in Eastern Europe through a reduction of credit availability as well.

FAULT LINE #7: SWITZERLAND

Another fault line which is quite worrying is in Switzerland. Swiss Daily Tagesanzeiger (4)has a good piece on this, which I have translated below:

A sovereign bankruptcy in Athens would hit the European banking sector with full force. Swiss banks in particular have invested heavily in Greece – for them, the risk is the greatest in Europe. But help is at hand.

The horror deficit of Greece is making the banks concerned. A failure to pay would hit first and foremost European institutions. “50 percent of foreign bank claims against debtors in Greece are to the Greek state. An Athenian bankruptcy would, therefore, hit other European countries and their banks hard, Citigroup strategist Giadi Giani said to the Financial Times Deutschland (FTD)."

In Greece, the fiscal situation is catastrophic. If the country does not find enough buyers for its bonds to reduce the deficit, it could lead to insolvency. Should no help come from EU countries or the IMF then, European banks would be threatened with massive writedowns, write the economists at Commerzbank.

Switzerland particularly affected

According to the International Monetary Fund (IMF), about two thirds of the debt of Greece is held by foreign creditors – an above average value. European Banks are particularly involved. According to data from the Bank for International Settlements, Swiss institutions, at around 68 billion francs, rank as one of the largest donors. Only the French banks, with 80 billion francs [of exposure] have stashed a bit more money in Greece.

But in relation to GDP, the risk to Switzerland, according to FTD, is the highest by far: According to Morgan Stanley economists [Swiss] commitment in Greece comes to almost twelve percent of Swiss GDP. France follows as the largest country in the eurozone at 2.5 percent.

FAULT LINE #8: EUROPEAN LENDING RATES

Bloomberg Reports:

A bailout of one will produce the same outcome as the rescue of Bear Stearns did; moral hazard will kick in, and instead of allowing economic Darwinism to cleanse the gene pool, the weaker nations will lose any incentive to cut spending and trim their swollen deficits.

Welcome to “Credit Crunch II.” By stuffing billions of dollars of taxpayers’ money into the balance-sheet holes of the banking industry, governments have transmogrified private risk into public liabilities. The “too-big-to-fail” label just reattaches itself to governments from financial companies.

The sequel, if the European Union or its members are suckered into some kind of Greek rescue package by buying, guaranteeing or even repaying its bonds, could end up featuring Portugal as Lehman Brothers Holdings Inc. and Spain as American International Group Inc.

Warren Buffett is often heard to say – “you find out who was swimming naked when the water goes out.”

European lending rates are headed higher. This will place further pressures on sovereign debt loads.

CONCLUSION

The apparent dithering of the ECB and the EC, along with the tremendous deficiencies in financial controls and audits of member countries, makes European leadership look empty headed. But maybe, just maybe the EU Boy is smarter than we think?

The apparent dithering of the ECB and the EC, along with the tremendous deficiencies in financial controls and audits of member countries, makes European leadership look empty headed. But maybe, just maybe the EU Boy is smarter than we think?

According to Martin Wolf writing in the Financial Times, what ails Europe is DEMAND. Without demand by consequence there emerges fiscal crisis. The Euro’s strength over the last 11 months has been the Euro Zones Achilles heel. Many pressured politicians felt a much weaker Euro would assist with increasing demand for European products and potentially alleviate some of the fiscal pressures. The problem needed to be fixed urgently and a weakened Euro was the immediate solution. A 10.3% devaluation of the Euro in 11 weeks is best described as dramatic and exactly what the doctor prescribed!

Is the Euro devaluation a byproduct of inaction or a strategy?

I will leave that debate to the academics and conspiracy buffs. (5)

"What if Greece is Fannie Mae, Portugal is Freddie Mac, Spain is AIG, Argentina is Wachovia Bank and Ireland is Lehman Brothers?" Bulls are certainly hoping Greece is more akin to Bear Stearns, whose Fed-engineered fire sale to JPMorgan in March 2008 sparked a brief but furious "relief" rally that spring”.

Todd Harrison, CEO of Minyanville.com.

Yahoo Finance 02-11-10

Dubai World is to Corporate Debt what Sub-Prime was to Consumer Debt

Greece is to Sovereign Debt what Dubai World is to Corporate Debt

Gordon T Long gtlong@comcast.net Web: Tipping Points

Mr. Long is a former executive with IBM & Motorola, a principle in a high tech start-up and founder of a private Venture Capital fund. He is presently involved in Private Equity Placements Internationally in addition to proprietary trading that involves the development & application of Chaos Theory and Mandelbrot Generator algorithms.

Gordon T Long is not a registered advisor and does not give investment advice. His comments are an expression of opinion only and should not be construed in any manner whatsoever as recommendations to buy or sell a stock, option, future, bond, commodity or any other financial instrument at any time. While he believes his statements to be true, they always depend on the reliability of his own credible sources. Of course, he recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction, before making any investment decisions, and barring that, we encourage you confirm the facts on your own before making important investment commitments.

© Copyright 2010 Gordon T Long. The information herein was obtained from sources which Mr. Long believes reliable, but he does not guarantee its accuracy. None of the information, advertisements, website links, or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. Please note that Mr. Long may already have invested or may from time to time invest in securities that are recommended or otherwise covered on this website. Mr. Long does not intend to disclose the extent of any current holdings or future transactions with respect to any particular security. You should consider this possibility before investing in any security based upon statements and information contained in any report, post, comment or recommendation you receive from him.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.