Chinese Money Supply - How Do You Say "Rube Goldberg" in Chinese?

Economics / China Economy Jul 21, 2007 - 01:36 AM GMTBy: Paul_L_Kasriel

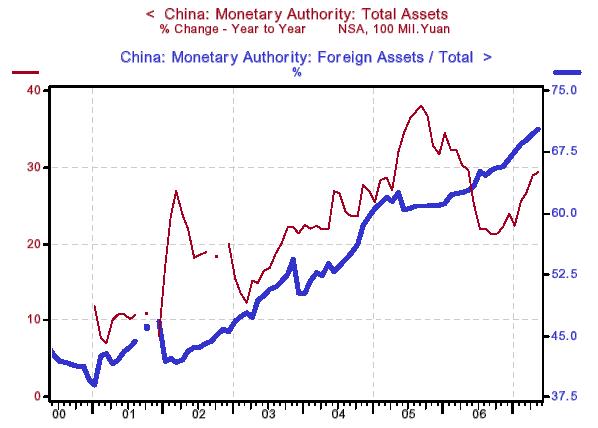

China has an economic problem - inflation. When I speak of Chinese inflation, I am referring to what the People's Bank of China (PBOC, not to be confused with PB&J) is doing - creating massive amounts of credit "out of thin air." Chart 1 shows that the total assets on the PBOC's balance sheet grew by approximately 29% in the 12 months ended May. Although that is down from peak growth of 38% in the 12 months ended September 2005, 29% still is a sizeable increase in central bank credit creation.

China has an economic problem - inflation. When I speak of Chinese inflation, I am referring to what the People's Bank of China (PBOC, not to be confused with PB&J) is doing - creating massive amounts of credit "out of thin air." Chart 1 shows that the total assets on the PBOC's balance sheet grew by approximately 29% in the 12 months ended May. Although that is down from peak growth of 38% in the 12 months ended September 2005, 29% still is a sizeable increase in central bank credit creation.

Chart 1

What is driving this rapid PBOC credit creation? Chart 1 also sheds some light on the answer to this question. The blue line in Chart 1 is the proportion of PBOC total assets that are foreign related. As of May, approximately 70% of PBOC total assets were foreign related. Because Chinese government policy is to manage the Chinese exchange rate, especially with respect to the U.S. dollar, and because the U.S. dollar "wants" to fall in the global foreign exchange market, the PBOC is forced to buy dollars in order to keep the Chinese yuan from rising faster relative to the dollar.

The PBOC pays for the dollars it purchases -- those dollars or the dollar-denominated investment instruments purchased with these newly-acquired dollars - showing up as foreign assets on its balance sheet - with Chinese yuan. And where does the PBOC get these yuan? The same place all modern central banks get their currencies - they create them with a stroke of a key. (One difference between central bankers and counterfeiters is that counterfeiters actually have to put a little work into creating currency - engraving and physical printing.)

What has been the result of all this PBOC inflation?

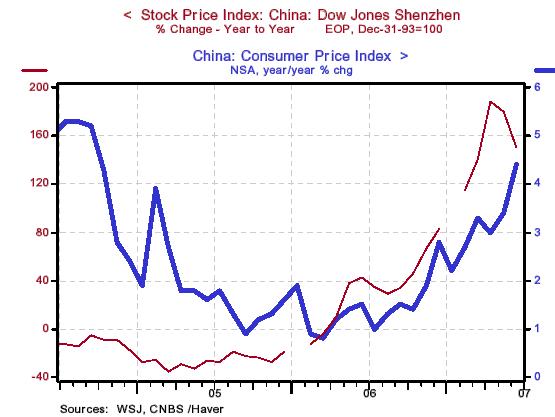

As Chart 2 shows, more rapid increases in the prices of consumer goods and services and corporate stock prices.

Chart 2

The Chinese government has become concerned about the pick up in the prices of Chinese goods/services and assets. It wants these price increases to slow down. If rapid growth in PBOC-created credit is what caused the acceleration in Chinese goods/services prices, then a slower growth in PBOC-created credit ought to calm things down.

So, did the Chinese government instruct the PBOC to cut back on its credit creation directly? No. The Chinese government has instructed the PBOC to raise interest rates on Chinese bank deposits (the Chinese still have a version of the old Fed Regulation Q) and the interest rates on bank loans. Also, in order to encourage Chinese citizens to hold onto the rapidly growing deposits, which have been created by rapidly growing Chinese bank credit, which has resulted from the rapidly growing PBOC credit, the Chinese government has cut the tax on interest earned on Chinese bank deposits. Talk about a Rube Goldberg approach to reining in central bank credit creation.

Not only is this a convoluted way to manage monetary policy, it is destined to fail. As long as the PBOC attempts to prevent the Chinese yuan from appreciating at its "natural" pace versus the U.S. dollar, the PBOC will be forced to continue inflating. As Milton Friedman, may he rest in peace, used to say, there are simple answers to problems but not necessarily easy answers.

By Paul L. Kasriel

The Northern Trust Company

Economic Research Department - Daily Global Commentary

Copyright © 2007 Paul Kasriel

Paul joined the economic research unit of The Northern Trust Company in 1986 as Vice President and Economist, being named Senior Vice President and Director of Economic Research in 2000. His economic and interest rate forecasts are used both internally and by clients. The accuracy of the Economic Research Department's forecasts has consistently been highly-ranked in the Blue Chip survey of about 50 forecasters over the years. To that point, Paul received the prestigious 2006 Lawrence R. Klein Award for having the most accurate economic forecast among the Blue Chip survey participants for the years 2002 through 2005.

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.

Paul L. Kasriel Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.