Dubai debt Defaults, Deflation In Action, Watched Pot Theory Revisited

Economics / Global Debt Crisis Nov 26, 2009 - 01:25 PM GMTBy: Mike_Shedlock

Last night after a 10 hour drive I was up at 5:00AM watching the futures plunge but not knowing why. Now we know: Dubai default fears spook investors

Last night after a 10 hour drive I was up at 5:00AM watching the futures plunge but not knowing why. Now we know: Dubai default fears spook investors

Global stock markets endured heavy selling on Thursday as investors were spooked by the spectre of a default by Dubai and after a febrile foreign exchange market saw the yen surge to a 14-year high against the dollar.

The turmoil caused a flight to less risky assets. Gold, which had challenged $1,200 in Asian trading, fell back from its highs and money flowed into havens such as German government bonds.

US markets are closed for the Thanksgiving holiday, but electronic trading of the benchmark S&P 500 equity futures contract showed a potential drop on Wall Street of 2.2 per cent.

As the European trading day progressed it became clear it was Dubai World’s difficulties that had hit a particular nerve, reminding investors of the lingering damage wrought by the financial crisis.

Banking stocks tumbled on concern about their potential exposure to Dubai. Indeed, the cost of insuring against default by the emirate jumped, with Reuters reporting the Dubai five-year credit default swap being quoted as high as 500-550 basis points. This means it would cost about $500,000 a year to insure $10m of Dubai’s debt. On Tuesday it would have cost about $360,000.

Greek and Irish government five-year credit default swaps also moved higher as nations with supposedly precarious fiscal positions were punished. In contrast, investors sought out comparative haven assets, pushing the yield on the German Bund down by 8 basis points to 3.16 per cent.

Dubai Debt Delay Rattles Confidence in Gulf Borrowers

Please consider Dubai Debt Delay Rattles Confidence in Gulf Borrowers

Dubai shook investor confidence across the Persian Gulf after its proposal to delay debt payments risked triggering the biggest sovereign default since Argentina in 2001.

The cost of protecting government notes from Abu Dhabi to Bahrain rose, extending the steepest increase since February as Dubai World, with $59 billion of liabilities, sought a “standstill” agreement from creditors.

Dubai World’s assets range from stakes in Las Vegas casino company MGM Mirage to London-traded bank Standard Chartered Plc and luxury retailer Barneys New York through asset-management firm Istithmar PJSC. The Dubai government’s attempt to reschedule debt triggered declines in stocks worldwide that had been rebounding from the worst financial crisis since the Great Depression.

Unlike Argentina, which stopped payments on $95 billion of debt eight years ago after yields on benchmark bonds more than doubled in four months to more than 40 percent, Dubai’s announcement yesterday “was a surprise,” said Alia Moubayed, a London-based economist at Barclays Plc.Gold And The Watched Pot Theory

While some were spouting US government debt default theories or dollar devaluation theories others were looking for the "unwatched pot".

Inquiring minds are taking another look at Gold And The Watched Pot Theory written October 07, 2009.

Message Of Gold

The reason for the strength in gold is not US inflation. As I have pointed out many times, gold fell from 850 to 250 over the course of 20 years, with inflation every step of the way. Thus, the inflation story just does not fit.

However, it should be clear that a major financial crisis is in store following a long period of competitive currency devaluation and massive debt and derivatives expansion by nearly every major country on the planet.

Might the US dollar blow up? Yes it might. But so could the RMB if China floated it, and so could the British pound. No one seems to see the crisis brewing in Japan with a huge demographic problem, a shrinking population, falling exports, and no way to pay back its national debt.

There is seldom a mention of the problems in European banks who foolishly lent money to the Baltic States in Euros or Swiss Francs and now those Baltic country currencies have collapsed and the loans cannot be paid back. European banks also lent to Latin America and those loans are also suspect. Arguably, European banks are in worse shape than US banks, but no one talks about it, at least in the US.

Spain has unemployment approaching 20% yet must suffer through the same interest rate policy as Germany. Seldom does one hear about this either.

Certainly the UK is a complete basket case with its banks on government life support. Iceland has already blown up, who is next?

Most are not aware of the problems in China, Japan, or Europe. However, the problems in the US are universally well understood. Indeed all eyes are on the dollar and everyone is talking about deficits, monetary printing, and especially unfunded liabilities even though the latter is tomorrow's problem, not today's.

Watched Pot Theory Revisited

A watched pot may boil, but it's not likely to explode, especially when everyone watching the pot expects an explosion any second.

Indeed, it would be fitting if the Ridiculous Hype Over Secret Oil Meetings, helped form a bottom on the US dollar.

Yet, it's easy to see that a financial crisis is brewing.

Somewhere, something is going to blow sky high, but from where I sit, it's as likely to be in the Yen, the Swiss Franc, the British Pound, or something no one is watching at all as opposed to the US dollar specifically.Hyperinflation?!

Amazingly some see this as hyperinflationary.

Nadeem Walayat writing for the Market Oracle says Deflationists Are WRONG, Prepare for the INFLATION Mega-Trend

Nov 18, 2009 - 12:58 AM

The jist of the deflationists argument is that debt deleveraging MUST trigger huge consumer and asset price deflation. Whilst we have all witnessed huge asset price deflation and some consumer price deflation during 2008 and into 2009. However we have also witnessed unprecedented government and central bank actions of this year, which have ignited asset price inflation with more to come that is now starting to feed into consumer price inflation.

Why do deflationists have it wrong ?

It is that focusing on the deleveraging of the the debt mountain is a red herring, taken on its own then yes it DOES imply deflation as the debt bubble 'should' contract. But given the asset price reaction of 2009 that is NOT what is actually taking place! the Debt bubble is NOT deleveraging, the bad debts are being dumped onto the tax payers! The huge derivatives positions that act as the icebergs under the ocean as compared to the asset price tips that we see above water are not contracting but expanding!

The DEFLATIONISTS ARE DEAD WRONG !

The last 8 months have proven it to be so ! But STILL they cling on as though they have blinkered visions as a function of presumably not having to put their own money on their deflation calls. What will there position be in another 8 months - it will be to REINVENT HISTORY TO IMPLY THEY SAW IT COMING ALL ALONG!What's amazing is how hyperinflationists who have blown the call for 10 years running now accuse deflationists in advance of rewriting history.

Here's the deal. Deflation happened, the only debate is how long it lasts. It is more than premature to proclaim the end of it on the basis of an 8 month period. Things do not progress in a straight line and a rebound after a 51% plunge in the S&P 500 and 10 year treasury yields close to 2% was expected.

That rebound is a much proof of the end of deflation as any of half a dozen 50-100% rebounds in the Nikkei over the last two decades, or the massive rebound in the DOW in 1931 before it plunged to new lows.

Many of those pointing to 8 month timelines as if that is what matters ignore an even bigger timeline in which stocks fell that 51%. If this rally is proof of inflation the the plunge must be proof of deflation.

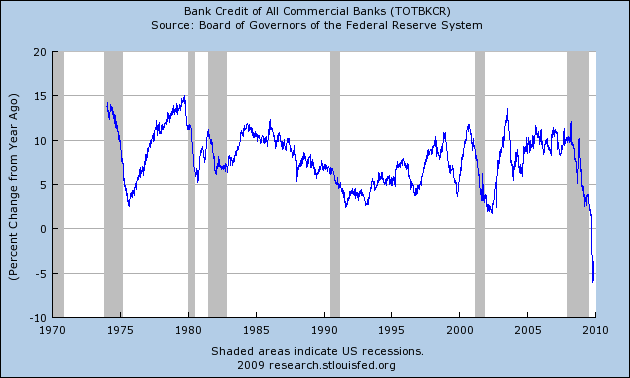

The reality is neither is true. What is true is that in a credit based fiat economy, what matters is ability of the Fed and Central Banks in general to foster bank lending. And that is not happening.

Total Bank Credit

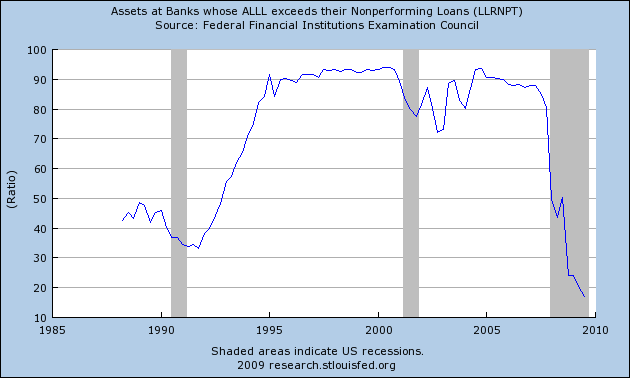

More Deflationary Writeoffs Coming

Allowances for loan losses will decrease as charge offs increase. However, the above charts are in relation to non-performing loans.

Because allowances for loan losses are a direct hit to earnings, and because allowances are at ridiculously low levels, bank earnings have been wildly over-stated.

The $trillions poured into the economy got a measly 2.8% rise in GDP.

Now what? Jobs are still contracting, businesses are not borrowing, banks are reducing credit card limits, etc, etc.

Those are not conditions of inflation, let alone hyperinflation. Now concerns are rising in Congress and the administration over the national debt. Meanwhile, more defaults loom: on housing, on commercial real estate, and on credit cards.

Two year treasury yields are at a record lows of .74 and five year treasuries are at 2.11.

If hyperinflation is coming, buy houses. Nowhere else can you get the leverage you can get in houses. It's a sure thing. Meanwhile I suggest gold has been rising for another reason: credit stress and fears of deflationary economic collapse.

Dubai just stepped up to the plate out of the blue, defaulting on debt. Defaults are part of the deflationary process. Prepare for more of them because they are coming.

I see no reason to change my stance that the US is in for a long slug of hopping in and out of deflation for quite some time. Ironically it is the hyperinflationsts who are rewriting history. The hyperinflationists had it wrong, deflation happened first.

Deflation is here, the only debate is how long it lasts. Some of us saw it coming, the rest still scream about the massive inflation that is supposedly coming. They may be correct eventually, but when?

By Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management . Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction.

Visit Sitka Pacific's Account Management Page to learn more about wealth management and capital preservation strategies of Sitka Pacific.

I do weekly podcasts every Thursday on HoweStreet and a brief 7 minute segment on Saturday on CKNW AM 980 in Vancouver.

When not writing about stocks or the economy I spends a great deal of time on photography and in the garden. I have over 80 magazine and book cover credits. Some of my Wisconsin and gardening images can be seen at MichaelShedlock.com .

© 2009 Mike Shedlock, All Rights Reserved

Mike Shedlock Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.

Comments

|

Nadeem_Walayat

26 Nov 09, 22:13 |

a Deflationist Lashing Out Nouveau Inflationists?

I have a great deal of respect for Mike so I will just make one single point, and that is my inflationary outlook is a NEW conclusion born out of current analysis that I am only now during November in the process of writing up as first a series of articles, which given the depth of evidence and complexity of trend projections the whole scenario will have to resolve into an ebook (that I will make available for free this year). Therefore the point is that I was never a hyperinflationist of any sorts, far from it, my analysis of key major market and economic trends correctly and accurately concluded in DEFLATIONARY outcomes that culminated towards a projected deflationary spike lower into Mid 2009 for asset and consumer prices such as the stocks bear market projected low of Dow 6,600 which was confirmed in March 2009 as the following excerpts indicate : Asset, Commodity and Consumer Price Deflation Projections : Aug 2007 - UK Housing Market Crash of 2007 - 2008 and Steps to Protect Your Wealth The UK Housing market is expected to decline by at least 15% during the next 2 years. Despite the 2012 Olympics, London is expected to fall as much as 25%. UK Interest rates are either at or very near a peak, as there is an increasingly diminishing chance of a further rise in October 2007. After which UK interest rates should be cut as the UK housing market declines targeting a rate of 5% during the second half of 2008. The implications for this are that the UK economy is heading for sharply lower growth for 2008. Jul 2008 - Crude Oil Parabolic Move Driven by Inflation Hedging that Could Unwind Crude Oil is well into a parabolic up move that has been driven higher by inflation hedging which had fed upon itself, the potential exists for a near imminent cascading mainstream interpretation of future economic conditions to suggest lower future inflation which would lead to a fast paced decline in oil prices targeting a move back towards the September 2007 breakout point of $80. With stop-gaps along the way of $135, $110, $100 and $85. Therefore I continue to remain bearish on the prospects for crude oil during the next 3 to 6 months or so barring a BLACK SWAN event. Oct 2008 - Stocks Bear Market Long-term Investing Strategy Current State of the Bear Market and Trend Conclusion The sum of the previous analysis suggests that we can discount a 1930's style wipeout of the stock market, and viewing a volatile sideways trend for at least the next 6 months to be followed by an gradual upward curve. In the meantime the credit chaos events will undoubtedly see much volatility that will see several spikes higher and lower in the 10% region, with a high probability that we will see the recent lows breached at least once between now and June 2009 as the most probable outcome is something that is reminiscent of the 1970's which suggests that the stock markets are headed towards the 2003 lows. Which given the recent sell off implies a further decline from recent lows in the order of 10%. Dec 2008 - UK CPI Inflation, RPI Deflation Forecast 2009 The UK is heading for real deflation during 2009 as the below graph illustrates in that the RPI inflation measure is expected to go negative and spike lower around June / July 2009 as the RPI is sensitive to falling mortgage interest rates. The CPI will also continue to fall sharply into May 2009, which is targeting a rate of just below 1%. However the more money the government borrows as the difference between spending and tax revenues then the greater will be the eventual resulting inflation as there is no such thing as a free lunch, that will reverse many of the trends we have observed during the past 6 months and will continue to see during virtually all of 2009. However I am only expecting a mild up tick in inflation late 2009 due to the deflationary nature of economic contraction. Jan 2009 - Dow Jones Stock Market Forecast 2009 In Summary, I do not know at precisely what price level the Dow will make a low during 2009, my best estimate at this time is 6,600, but I am expecting that it will mark the start of a multi-year bull market that will eventually make 2008-2009's price action appear as a mere minor blip, much as the 1987 crash appears on today's price charts. Feb 2009 - UK Recession Watch- Britain's Great Depression? In the final analysis, the projected course of the recession over the next 2 years is as illustrated by the below graph in that the severe recession is expected to bottom at an annualised rate of -4.75% GDP in the fourth quarter of 2009 (small quarterly gain on the 3rd quarter), which will be followed by a recovery as the rate of annualised GDP contraction improves as government stimulus measures announced to date and deep interest rate cuts as well as future stimulus during 2009 kick into gear. The UK economic recovery is expected to continue into the fourth quarter of 2010 i.e. after the general election. The total recession from peak to trough is expected to see GDP contract by 6.3% and therefore this will be the worst recession since the 1930's Great Depression. Mar 2009 - Stealth Bull Market Follows Stocks Bear Market Bottom at Dow 6,470 In Summary - We have in all probability seen THE stocks bear market bottom at 6470, which is evident in the fact that few are taking the current rally seriously instead viewing it as an opportunity to SELL INTO , Which is exactly what the market manipulators and smart money desires. They do not want the small investors carrying heavy losses of the past 18 months to accumulate here, No they want the not so smart money to SELL into the rally so that more can accumulated at near rock bottom prices! Therefore watch for much more continuous commentary of HOW this is BEAR MARKET RALLY THAT IS TO BE SOLD INTO as the Stealth Bull Market gathers steam. Sep 2009 - UK Inflation Forecast, Will RPI Deflation Return to Inflation?

The trend into Extreme UK Deflation as measured by RPI has come to an end, forward inflation is expected to rise at a subdued rate as result of the economic recovery into the 2010 general election with RPI targeting +1% so Yes RPI Deflation will come to an end, but thereafter the high risk of a double dip recession expectation suggests the shallow uptrend in inflation will come to a halt during 2010 despite further quantitative easing and arm twisting of the banks to LEND into 2010 as the Bank of England attempts to increase the velocity of money by all means with even the option of negative interest rates to force the banks to take risks rather than park their tax payer bailout money at the BoE to earn risk free interest on. However as i warned in November 2008 Bankrupt Britain Trending Towards Hyper-Inflation?, that Britain could be put on to the path of hyper inflation if it proceeded to follow the mainstream academic economist suggestions of printing money to monetize debt in ever escalating amounts as a consequence of the deficit spending and bailing out of the bankrupt banks, which is the path that Britain has subsequently embarked upon during 2009. Britain is Not bankrupt and not likely to go bankrupt in the immediate future, however Britain is on the path towards Bankruptcy if it goes on the projected borrowing spree that lifts real debt to £3.2 trillion and is forced to take on banking system liabilities of £5 trillion, under such a situation the country would be bankrupt as the currency would collapse, and we would not be able to service the debt much of which would be denominated in foreign currencies given Britain's position in the global financial system. Though the more probable outcome of stagflation for many years (low economic growth, high inflation and interest rates) that erodes the value of domestic debt and savings would in itself be a bad outcome for Britain. The only real solution is to limit the growth of real public debt by cutting back on public spending and bringing public sector pensions inline with the private sector, both of which will be positive signals to the UK debt market and banking system. I suspect today's deflationists will eventually be forced into changing their views over the coming years in the face of the failure of expected trends to materialise, just as a 60% stocks rally occurred whilst some die hard deflationists focus remained fixated on the preceding 51% drop. For more on my NEW INFLATIONARY scenario, ensure your subscribed to my always free newsletter to get the full implications in your in box as it will be one of my seminal pieces much more so than even the Stocks Stealth Bull Market Scenario of March 09 and Crude Oil Top of July 08, or the UK Housing Market August 07 Top and Bear Market were before it amongst many others. By Nadeem Walayat Copyright © 2005-09 Marketoracle.co.uk (Market Oracle Ltd). All rights reserved. |